Like the skies above Parliament House — and many of the people inside it — the economic forecasts in this year’s budget look pretty dismal. Unemployment will stay above 6% over the forward estimates, and the economy will grow by a lukewarm 2.5% this year, edging up to 3.25% in 2016-7.

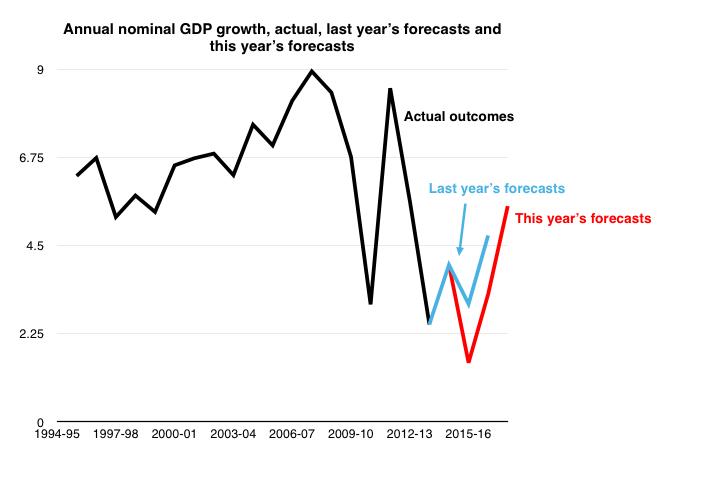

Once again, one of the most important economic numbers in the budget is nominal GDP — that is, real economic growth, plus inflation. Nominal GDP matters because it’s the base on which the government levies tax.

Here, the news is not so good. In last year’s budget, nominal GDP was supposed to grow by 3% this year and 4.75% the year after; in this year’s budget, Treasury is predicting growth of an anemic 1.5% this year and 3.25% the year after. It could be even worse, given that Treasury has consistently overestimated nominal GDP growth since the global financial crisis. This is largely being driven by what has by now become the most reliable of villains: a falling iron ore price. The average price per tonne in this budget is $48, exactly half what it was last year and $12 a tonne down on the last Mid-Year Economic and Fiscal Outlook.

Partly this is driven by a shift in Chinese growth, but part of it is the mining sector’s own fault. Massive investment in mining capacity has the potential to lead to what economists call “immiserating” growth: we’re producing more iron ore, but that increase in supply will tend to push the price of iron ore down, meaning that we may be receiving less money overall even though we’re exporting more. The budget papers describe Australia as “leading the way” with an extra 50 million tonnes of capacity coming online in 2015: this might not be a race that it’s in our interests to win.

Falling international coal prices are somewhat glossed over. Treasury’s forecasts for the terms of trade are driven by the assumption of a metallurgical coal price of $90 a tonne (down from around $130 a tonne in last year’s budget) and a thermal coal price of $60 a tonne (down from about $80 a tonne last year).

There are, apparently, some bright spots on the horizon: notably, Treasury is counting on the fact that with the dollar, interest rates and fuel prices all down, businesses will be inclined to spend money on things that aren’t destined for the mines. But, as the papers point out, so far, there hasn’t been any sign in ABS investment expectation statistics that businesses are getting ready to open their wallets. They’ll certainly need to if they’re going to offset the huge declines in mining investment, which will drag down GDP growth by a cumulative 4 percentage points in the next few years.

Budget time is when the government likes to pretend that it’s in control of the economy. But developments in the global economy drive what happens domestically.

The government is betting big on Narendra Modi’s new government in India: Treasury — in line with the IMF — has bumped up its forecasts for Indian real GDP growth from the 4% or so in last year’s budget to 7.5%. There has been some controversy recently about the accuracy of Indian economic statistics, but there’s no doubt that, if Modi can ram his tax and land acquisition reforms through the Indian Parliament, growth is likely to pick up there. The government is currently pursuing a preferential trade agreement with India, and the budget is dutifully hyping the potential for growth in trade and investment links between Australia and India — but, as with the trade agreements signed last year, it’s hard to see how another more or less toothless bilateral will have much of an impact on either trade or growth.

(As an aside, this budget has taken the now established political convention of describing anything — spending, taxes foregone, the price of fish in Estonia — as “investment”; thus, the tariff revenue that will no longer be collected on imports from China, South Korea and Japan is described as an “investment” in the trade agreements.)

China’s growth has been taken down a few notches, while Europe has ticked up a bit. The very real and potentially very damaging Greek exit from the eurozone is described, in an exquisitely artful bit of bureaucratic euphemism, as “recent developments” that “highlight the continued structural challenges faced by the euro area”.

Those of you who put your faith in the G20’s Brisbane Action Plan to raise global GDP by 2% (here’s looking at you, Joe Hockey) may be disappointed to learn that overall, world GDP growth will in fact be slightly lower this year than was forecast last year, before the Brisbane Summit. If anything, this furnishes a nice little story about the impotence of modern governments: it’s easy to talk a good game about your “economic plan” lifting growth, but Australia is a fairly small boat in a pretty turbulent ocean. It’ll be tough sailing for a while yet.

Eureka!!!!! An article which actually addresses important economic issues. I’ve posted it in Microsoft Word so I can re-read it at my leisure.

Well done.