While foreign-owned companies are likely to benefit from a cut in the company tax rate, Australian investors are likely to see no difference.

In the budget earlier this month, the federal government outlined plans to cut the company tax rate over the next 10 years from 30% to 25%. The Australia Institute (TAI) estimates this will give Australia’s top 15 listed companies $58 billion over 10 years from July this year. Today, TAI has released a report (covered elsewhere in Crikey) stating that the money US companies save by paying less tax in Australia will actually go to the US’ own Internal Revenue Service, as US-domiciled companies that operate abroad have to pay the IRS the difference between the US company tax rate and other countries’ company tax rate.

For Australian shareholders, however, it is a different story.

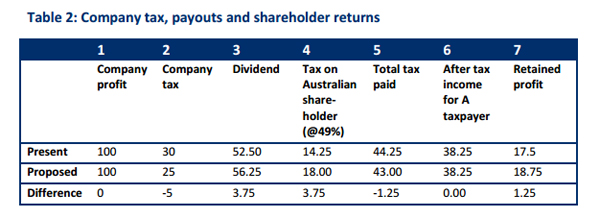

Australian shareholders receive a credit for the company tax paid by the company they have shares in against their own income tax liability via a scheme called dividend imputation.

For example, fictitious company Agile and Innovative Pty Ltd earns $100 million in pre-tax profit, and after company tax has $70 million in profit. It offers that as a dividend to shareholders such as Samantha, who gets $70 in return. She also gets a franking credit of 30% because of the tax paid. This means that whatever tax rate Samantha is on, the franking credit counts as tax already paid. If she’s on an income tax rate below 30%, she’ll get a refund, but if she’s on a tax rate higher than 30%, she’ll have to pay the difference up to her tax rate.

If the company tax rate is lowered by the government, that will reduce the offset the shareholder gets on his or her own income tax liability. The Australia Institute’s David Richardson demonstrated this in an earlier paper late last year before the government’s policy was announced, and noted that there would be very little incentive for the owners of the company to put that funding back into investment if their own tax paid has changed very little.

“Clearly as far as the owners of the corporation are concerned nothing has really changed. Because of this it is hard to imagine that the ultimate company owners would have any increase in the incentive to invest or innovate.”

The Australia Institute says that the only potential beneficiaries to a cut to the Australian company tax rate are foreign shareholders, but even for them, the change is likely to be very limited, due to double taxation agreements Australia has signed up to. This means that income tax paid in Australia goes out as a credit on tax paid in the home country of the shareholder. So, as with the United States, any change to Australia’s company tax rate is likely to be eaten up by tax in other countries.

So that leaves Australians who hold their wealth in low-tax offshore accounts as the only winners …

Who would have thunk it?