The claim

Renewable energy advocates have long argued that governments should dump taxpayer support for fossil fuels and embrace cleaner technologies.

During a recent episode of the ABC’s Q+A, an audience member suggested the deck was stacked against clean energy, with the equivalent of US$29 billion a year handed out to subsidise “fossil-fuel extraction and production of energy”.

But that was rejected by National Party senator Matt Canavan, who didn’t accept the premise of the question, or the figures.

“There’s no subsidisation of Australia’s fossil-fuel industries,” he said.

Does the government not subsidise Australia’s fossil-fuel industries? RMIT ABC Fact Check investigates.

The verdict

Canavan draws a long bow.

There are many ways to define “subsidisation”. The Q+A audience member who questioned him cited figures from a 2019 International Monetary Fund (working paper which found fossil fuels in Australia received US$29 billion in subsidies in 2015.

That study relied on a very broad definition of “subsidy”, counting among other things social and environmental costs typically not borne by fossil-fuel producers such as localised pollution, greenhouse gas emissions and traffic congestion.

Other definitions are narrower, focusing on direct or indirect transfers from governments to producers or consumers to encourage production or consumption.

Even on a narrower definition, Australian fossil fuel producers are to some degree “subsidised” by federal and state governments, with a range of budget spending programs, tax concessions and other forms of assistance on offer.

Fossil-fuel companies receive fuel tax credits for excise paid on fuel they use, tax breaks for exploration, and accelerated depreciation for capital spending, as well as state spending to encourage specific projects among other benefits.

Untangling the web of federal and state taxation and spending programs is difficult, as experts conceded.

And while there is disagreement about whether all such benefits should be counted as subsidies, it is a stretch to argue there is “no subsidisation”.

Whether such benefits are in the public interest, or whether the renewable sector is subsidised to a greater or lesser degree, are different questions, and not the subject of this fact check.

What is a subsidy?

In broad terms, subsidies can involve directly or indirectly using public finances, public resources or regulatory mechanisms to lower production costs, thereby encouraging production to be higher than it otherwise would have been.

Subsidies can also directly or indirectly target consumers with incentives to encourage consumption.

In 2019 the United Nations environment program recommended measuring fossil-fuel subsidies according to the definition contained in the World Trade Organisation’s agreement on subsidies and countervailing measures. It said this was “the most widely recognised” internationally.

The agreement states that a subsidy exists when a government provides “a financial contribution” that confers “a benefit”.

It specifically covers: direct payments; forgone revenue (for example fiscal incentives such as tax credits); providing goods or services; any support from income or price regulation.

The fossil-fuel industries

The Organisation for Economic Cooperation and Development defines fossil fuels as simply “coal, oil and natural gas”.

“By extension,” the International Energy Agency explains, “the term fossil is also applied to any secondary fuel manufactured from a fossil fuel.”

Fact Check will assume fossil fuels include coal, oil and natural gas, as well as secondary fuels such as petrol and LPG.

Canavan made his claim about the “fossil-fuel industries” in response to a question about “fossil-fuel extraction and [the] production of energy”.

Energy generation relies on the consumption, rather than production, of fossil fuels. However, fossil fuel-fired power is often included when fossil fuel subsidies are measured.

In fact the UN environment program report explicitly recommends it, since “[s]ubsidies for electricity and heat generated from fossil fuels incentivise overconsumption of fossil fuels”.

Fact Check has briefly considered some forms of government assistance that apply to fossil-fuel electricity generation, bearing in mind that the term “fossil-fuel industries” is somewhat difficult to define.

Surrounding context

As mentioned, Canavan was asked about a 2019 report by the IMF examining subsidies for fossil fuels and fossil-fueled electricity.

The US$29 billion figure reflects the gap between what consumers pay for fossil fuels and what they would theoretically pay if prices reflected three things: the full cost of supply; consumer taxes; the cost of “adverse effects on society”.

Consequently the IMF counts “negative externalities” in its definition. These are costs imposed on society and the environment that are typically not borne privately by fossil-fuel producers, including traffic congestion, road accidents, localised air pollution and greenhouse gas emissions.

However, the UN environment program report found the IMF’s approach was “not widely accepted”.

Chief executive of the Centre for International Economics David Pearce told Fact Check it was hard to say who was benefiting from such a “subsidy”:

“If I’m driving my car using fossil fuels but I’m not paying a tax for that, who’s getting the subsidy?” he says.

Canavan rejected the IMF figures and its approach: “I don’t accept the facts that were put in the question.”

He suggested a better arbiter on the question of fossil-fuel subsidies was Australia’s Productivity Commission, a government-funded research and advisory body.

“I think the Productivity Commission here locally knows a lot more about the subsidies given to our different industries,” he said. “And they have rejected that.”

What the Productivity Commission actually says

The Productivity Commission’s trade and assistance review provides an annual snapshot of tariffs, subsidies and tax concessions across various industry groupings.

But as the commission says in its 2018-19 review, its estimates “do not capture all Australian support to industry”.

“The commission’s assistance estimates cover only those measures that selectively benefit particular firms, industries or activities, and that can be quantified given practical constraints in measurement and data availability,” it says. “Consequently, there are some significant government programs that selectively confer industry assistance, but cannot be appropriately estimated.”

The commission, for example, does not measure the effects of government spending preferences, regulations or arrangements with a “broader public objective” but which may benefit particular industries, such as transport infrastructure.

And it only considers federal subsidies, although it notes that state and territory government assistance — to the primary production and resources industries in particular — “has been considerable”.

As a result, the report says its estimates “do not cover the full extent of assistance to industry and the gap between reported values and actual assistance is potentially large”.

Nor does the commission provide a specific breakdown of support provided to “fossil-fuel industries”. As the commission told Fact Check in an email: “The commission does not have a breakdown of subsidies (or budgetary assistance) for the fossil-fuel industry in its trade and assistance review (TAR), but does produce estimates for tax concessions and outlays for mining and the [manufacturing] industry subdivision of petroleum, coal, chemical and rubber products.”

The annual review also contains a relevant subdivision of the services industry: “electricity, gas, water and waste”.

Each of these three classifications covers more than just fossil-fuel companies.

For these reasons, the commission’s figures do not allow an accurate assessment of subsidisation of “fossil-fuel industries”.

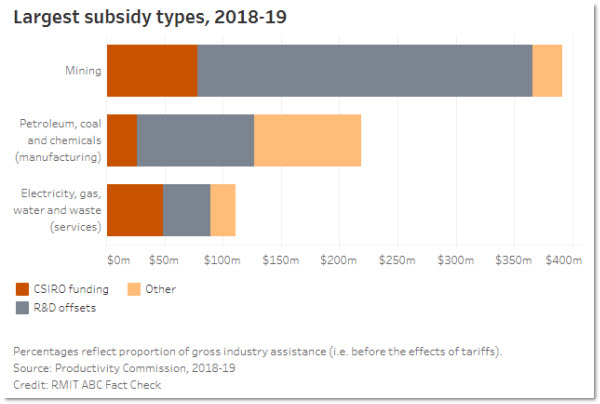

In net terms, the commission’s latest report shows the federal government provided about $12 billion in subsidies across all industries in 2018-19.

Of that the mining industry received $335.5 million; the manufacturing industry subdivision of petroleum, coal and chemicals received $384.6 million; the services industry subdivision of electricity, gas, water and waste received $90.3 million.

These net figures account for the effects of Australian border tariffs, both positive and negative.

As the graph below shows, as a proportion of gross assistance the bulk of those subsidies came in the form of tax offsets for research and development or funding to the CSIRO.

That funding would cover, for example, the Mining Geoscience Team, which the agency says among other things contributed towards “improving … productivity in the mining industry”.

As noted, it is difficult to unravel the level of fossil fuel subsidisation from the commission’s figures.

However, the figures do suggest that at least to some extent fossil-fuel industries receive government support that could be considered “subsidisation”.

Another approach is to examine some specific measures available to fossil-fuel producers.

Fuel tax credits

These credits are paid to refund fuel excise or customs duty paid on fuel used in vehicles or machines that do not operate on public roads. As the Australian Taxation Office explains, the amount depends on the type of fuel, when it was purchased and what it is used for.

Tax Office figures for 2017-18 show that fuel tax credits are claimed by companies across all industries.

Coal mining was the single biggest beneficiary, accounting for roughly $1 billion (15%) of the $6.8 billion total. The oil and gas extraction industry accounted for a further $110 million.

There is, however, some debate as to whether the credits represent a “subsidy”.

The justification for the rebate is that many users of big vehicles or machines don’t use the roads and therefore should not pay fuel taxes ostensibly imposed to pay for public roads.

This argument was made by Canavan on Q+A. He said the credit was to refund fuel taxes paid by businesses not using the road system.

“The idea being that the petrol tax you pay at the pump is to help pay for our roads, but obviously the big trucks in our mines are operating off-road and on roads that they have paid for,” he said.

The Minerals Council has also argued that the credit should not be considered a subsidy.

This argument assumes that fuel excise represents a genuine “hypothecated” tax that should not be borne by non-road users, rather than a broader revenue raising tax imposed by the federal government.

The OECD’s inventory of support for fossil fuels, however, treats Australian fuel tax credits as a subsidy.

It notes “the mining sector is a prime beneficiary” of these credits, so “the measure could arguably be considered producer support since it lowers the cost of inputs used in the coal-mining and hydrocarbon sectors”.

At the very least, the rebate serves to cut the cost of fuel inputs for fossil-fuel industries, representing a transfer from taxpayers in the form of forgone revenue that effectively lowers the cost of production.

Director of the Tax Group at Melbourne University law school Professor Miranda Stewart said in her view the fuel tax credit represented a subsidy.

“The diesel fuel rebate reduces the cost of fuel business inputs for mining and agriculture, which are some of our largest emitting sectors, and this enables them to sell ultimately to export and domestic markets at cheaper prices so in this sense, there is a subsidy,” Stewart says.

Research and development tax incentives

Another significant transfer to the fossil-fuel industry comes in the form of the research and development tax incentive.

As with the fuel tax credit system, the question of whether the incentive — offering a tax offset for research and development activities — constitutes a “subsidy” is disputed.

The argument for the incentive is that research and development has broader economy-wide benefits that extend beyond the private interests of individual businesses.

The tax offset is designed to recognise this.

Pearce said subsidies were usually designed with specific policy objectives in mind, but the “unintended consequences” of a policy such as tax concessions for research and development could be “that you do end up subsidising a particular industry relative to others”.

Productivity Commission data shows the mining sector (which as mentioned includes some but is not limited to fossil-fuel producers) benefited to the tune of $288 million in 2018-19.

Coal, petroleum and chemical businesses collectively received $101 million in 2018-19. Electricity, gas, water and waste businesses claimed a further $41 million.

Although the tax break is widely available and designed to encourage research and development with economy-wide benefits, it too arguably fits the definition of “subsidisation”, given it results in forgone revenue directly lowering costs for private companies.

Smaller measures

Fossil-fuel producers also received other smaller payments that were included in the Productivity Commission’s figures that could be regarded as subsidies. For example, mining received $9.3 million in 2018-19 to encourage small companies to conduct mineral exploration, including for fossil fuels.

Electricity, gas, water and waste services received $8.9 million for the carbon capture and storage flagship program, which the government says funded the investigation of a potential storage network to capture carbon dioxide from “industrial plants or power stations”.

Before its 2019 budget, the federal government announced $10 million in funding for “reliable energy infrastructure” (also mentioned in this fact sheet).

This included funding of up to $4 million to a private energy company to conduct a feasibility study into a coal-fired power plant in the Queensland town of Collinsville.

Other tax breaks

A briefing note from ANU’s Tax and Transfer Policy Institute, co-written by Curtin University PhD candidate Maria Sandoval-Guzman and Stewart, said subsidies for fossil-fuel companies are built into Australia’s tax law.

These include an immediate tax deduction for expenditure on prospecting and quarrying, and faster depreciation of assets in specific industries — namely gas supply, oil and gas extraction, petroleum refining and the primary production sector.

Each year Treasury produces a tax benchmarks and variations statement that estimates how much “revenue the government doesn’t collect” due to “provisions in the tax system that apply an alternative treatment of particular taxpayers or forms of economic activity”.

Its 2019 statement showed that deductions for prospecting and quarrying cost taxpayers $200 million in 2018-19. Meanwhile, the cost of faster depreciation was either too small or not possible to estimate.

State incentives

Critically, Canavan did not distinguish between state and federal subsidies, referring only to “subsidisation”.

As noted, the Productivity Commission’s report only considers federal subsidies. However, the states also allocate funding to fossil-fuel industries in a manner that could be considered subsidisation.

For example, the Queensland government has announced spending to expand the Abbot Point coal terminal to facilitate coal exports from the Galilee Basin.

The state’s 2016-17 budget papers make clear that this work was dependent on Adani’s Carmichael coal mine proceeding.

Fact Check has not considered state spending on fossil-fuel industries in detail, except to reiterate the commission’s position that previous state and territory assistance to industry “has been considerable”.

Although more recent calculations are not available, the commission found, for example, that state and territory governments’ assistance to industry amounted to about $4 billion in identifiable assistance in 2008-09.

It said this equated to around $184 a person, of which about 60% went to the primary production and resources industries.

More from the experts

Pearce said Australia had a complex set of tax and administrative arrangements that can be “quite hard to really finely unpick”.

However, even on the Productivity Commission’s own numbers, fossil-fuel producers are “almost certainly being subsidised”.

“Just to a much smaller amount than the numbers you’re going to get from the IMF,” he said.

University of Queensland professor of economics John Quiggin adopted a broader definition of “subsidy”, more closely aligned with the IMF report.

“By far the most important subsidy of the fossil-fuel industry is the absence of a carbon price,” he says.

“If we had a carbon price that reflected the social cost of CO2 emissions, generating electricity with fossil fuels would be uncompetitive compared to new solar and wind, with storage.”

Melbourne University economics professor John Freebairn said it was difficult to “square the circle” in terms of a reasonable definition of “subsidisation”.

Freebairn said most of the tax benefits available to fossil-fuel companies such as research and development tax concessions and accelerated depreciation of some assets were available to other industries.

Tthe private costs and benefits faced by fossil-fuel producers was “pretty close to a level playing field” compared to producers in other industries such as manufacturing.

In their briefing paper, Sandoval-Guzman and Stewart said arguments against transitioning away from coal, mining and gas into renewable energy often centred on the impact on employment.

They argue that government spending could be redirected from tax subsidies for fossil fuels — such as accelerated depreciation for polluting heavy vehicles or equipment, or fuel subsidies — towards transitional job support, retraining schemes and strengthened regional industries in renewables.

Principal researchers: David Campbell, senior researcher and Josh Gordon, economics and finance editor

Sources

- Matt Canavan, Speaking on Q&A, June 1, 2020

- IMF, Global fossil fuel subsidies remain large: An update based on country-level estimates, May 2, 2019

- UN Environment Program, Measuring fossil fuel subsidies in the context of the sustainable development goals, 2019

- Carbon Brief, Explainer: The challenge of defining fossil fuel subsidies, June 12, 2017

- WTO, Agreement on subsidies on countervailing measures, 1994

- OECD glossary of statistical terms, November 12, 2001

- IEA, Energy statistics manual, November 8, 2004

- Eurostat, Statistical glossary, September 9, 2019

- IMF, Reforming energy subsidies, summary note; accessed July 27, 2020

- Productivity Commission, Trade and assistance review 2018-19

- Department of Industry, Science, Energy and Resources, Research and development tax incentive; accessed July 27, 2020

- Department of Industry, Innovation and Science, Budget portfolio statements, 2019-20

- ATO, Fuel tax credits — business; accessed July 27, 2020

- ATO, Taxation statistics 2016-17, Excise — Table 4 (Fuel tax credits scheme for 2006-17 to 2017-18), November 11, 2019

- Parliamentary Library, Research paper: petrol and diesel excises, October 3, 2000

- Minerals Council of Australia, Media statement: Australian mining not subsidised by taxpayers, June 26, 2019

- OECD, Inventory of Support Measures for Fossil Fuels, 2019

- ATO, Greenfields mineral exploration initiative, August 30, 2017

- ATO, Product stewardship for oil program, December 21, 2018

- Department of Industry, Science, Energy and Resources; Carbon capture and storage flagships, February 28, 2020

- Scott Morrison, Media release: Delivering affordable and reliable power, March 26, 2019

- Australian Government, Fact sheet: Securing energy affordability for commercial and industrial users; accessed July 27, 2020

- Angus Taylor, Media release: Backing reliable energy for commercial and industrial users, February 8, 2020

- Miranda Stewart & Maria Sandoval-Guzman, Tax and Transfer Policy Institute briefing note: tax and energy, May 2020

- Treasury, 2019 Tax Benchmarks and Variations Statement, January 2020

- Queensland Government, Budget Paper 3, 2016-17

- WTO, World Trade Report (Defining Subsidies), 2006

- IEA, OPEC, OECD and World Bank, Analysis of the scope of energy subsidies and suggestions for the G20 initiative, June 6, 2010

- OECD-IEA, Update on recent progress in reform of inefficient fossil-fuel subsidies that encourage wasteful consumption, April 2019

- UN SDG indicators, statistical database (2017)

- Henry Tax Review, Final Report, 2009

- Jeremy Moss, Matt Canavan says Australia doesn’t subsidise the fossil fuel industry …, June 3, 2020

- Australia Institute, Mining in the age of entitlement, June 2014

- ODI, G20 subsidies to oil, gas and coal production: Australia, November 2015

I don’t understand why the verdict is a long bow, it seems conclusive to me that there is a lot of subsidy by any definition.

The verdict agrees with you: “Canavan draws a long bow.”

That is a prime example of a “fact check” defined and applied to produce a result acceptable to the “checkers”.

When I worked for CSIRO, the Environmental Divisions were required to get substantial industrial funding in order to do research. The Mining Division did not, and was not required to, seek industrial funding.

What do you expect – Canavan learned all his politics at the knee of the master – Cousin Jethro.

Please readers, don’t ever forget that Canavan’s ally Morrison heavily subsidised fossil fuel when he displayed and passed around a piece of coal in OUR PARLIAMENT saying that coal is friendly and won’t hurt you.

Can we have a reply from Mr Canavan?