Cigarettes or mobile phones? What’s your poison?

People can be addicted to either, and which you have chosen makes an enormous difference to the prices you face. Tobacco prices are up almost 20-fold, while the price of audio-visual and computer equipment has fallen by almost the same amount

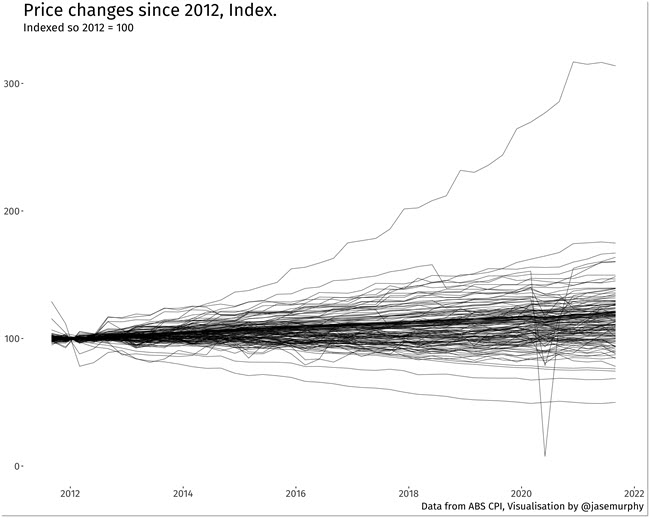

The latest consumer price inflation data came out this week and showed prices rose 3% over the last year — i.e. the average item that cost $1 a year ago costs $1.03 now. That seemingly moderate number was enough to have economists freaking out and sent markets into a frenzy. But the 3% average hides a very diverse range of outcomes for individual items.

The next chart shows all the items in the consumer price index over the past nine years. While price rises cluster around moderate growth, there are a few items that have become dramatically more expensive, and a happy handful that are far, far cheaper.

What are those expensive items? The number one riser is tobacco. Thanks to a world-leading tax regime, the price of a pack of cigarettes has risen at an astonishing rate since 1990: up over 1700%.

We have discussed in these pages how price rises in tobacco mean smokers bear the brunt of inflation, and the moral ambiguities of loading up society’s least capable with hefty price rises. To the extent it deters smoking, it’s great, but when it doesn’t, tobacco tax just depletes the remaining resources of people who can least afford it.

The second biggest riser on the list, ironically, is health. Healthcare is 500% more expensive than it was in 1990 — noting that this covers only those items that cost money, like GP co-pays, private care, etc. Medicare means a public hospital trip should still cost us a nice round $0.

Third on the list is the category of alcohol and tobacco combined. Fourth is medical and dental combined. Fifth is insurance. Like electricity, which is seventh, this is an essential. We can choose not to smoke. But the cost of power and insurance are things we can’t dodge.

Education is in sixth place. Private education costs a motza and the price of university has gone up as fees have risen, but public primary and secondary schools are still out there educating children for no or minimal fees.

Utilities round out the list. Energy is expensive and you can see why household bills are so often a political touchpoint — they are getting heftier and heftier.

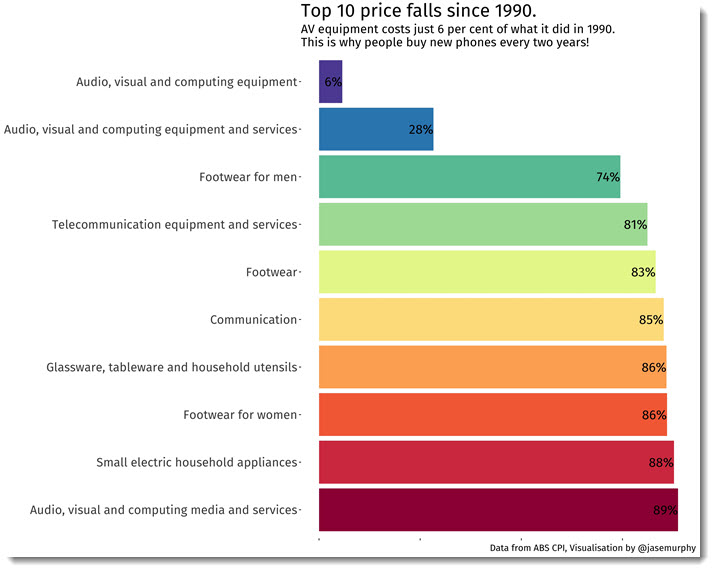

But price rises are not the only story of inflation. If they were, inflation would not be just 3%. Some items do fall in price.

As you can see, electronics top the list. Footwear is also prominent. It is tempting to look at this list and conclude that the falls are in categories that are less important than the categories where prices are rising.

But beware getting the causation around the wrong way. We consider shoes boring because they are cheap. They are certainly vital (albeit perhaps less as we work from home). The fall in prices make these categories far less salient when we think about our household budgets.

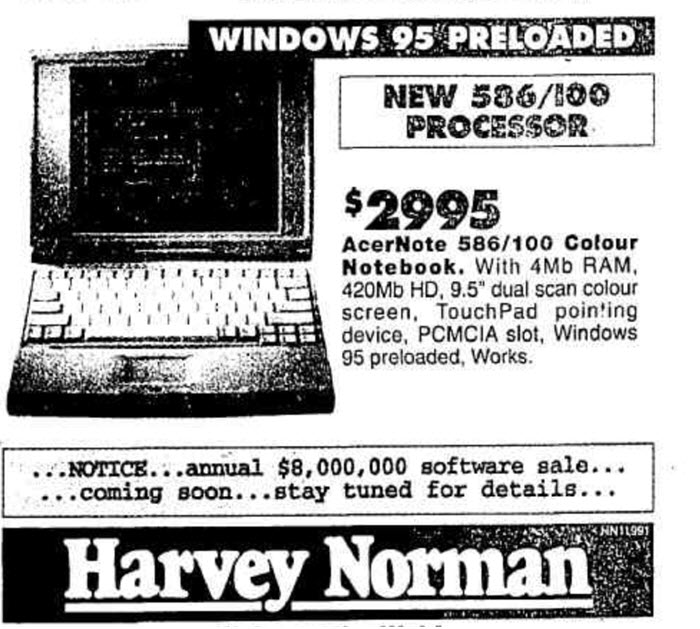

An equivalent computer would cost about 10% of this today.

This is perhaps why so many people believe inflation is out of control even as the data shows us it is moderate — prices which rise are highly noticeable. We sweat on categories where prices are rising.

Even technology CEOs who give away their products for free can believe the world is experiencing hyperinflation. The following example comes from the chief executive officer of Twitter, Jack Dorsey:

Higher inflation is a risk as supply chain constraints bite. But hyperinflation? We shall see. The big picture suggests price rises will be moderate as long as countries are trying to escape poverty through manufacturing.

Things which are falling in price are overwhelmingly manufactured goods — mostly imports. Things that are rising in price include services and other things we can’t import, like electricity.

The global attenuation in inflation since the 1970s is almost certainly explained in part by the rise of manufacturing in East Asia. As countries like China and Vietnam grow richer, the baton has been passed. Places like Ethiopia have become hubs for fast fashion production.

But can the cycle continue forever? If we run out of countries that have low enough wages to continue to make things cheaply, we could be seeing a lot more items vying with tobacco for first place on the list of price rises.

What about the cost of housing?

Exactly, significant house inflation in recent years, especially major cities, which should be central to assessments of consumer spending and affordability. However, one is suspicious of headline or nominal price obsessions (sometimes adjusted for CPI) that mask long term costs of property i.e. real value can be in decline due to sustained periods of stagnation pre Covid.

Then there is a trap for any government including the ‘weaponised’ financial asset that homes have become, in the CPI basket, because it would increase the CPI significantly, then require higher interest rates to dampen demand, then hit the ‘real economy’; vicious cycle.

to quote Prof Bill Mitchell ‘The CPI rose by 0.8 per cent in the September-quarter 2021 and 3 per cent over the 12 months. The two main drivers were the rise in prices for New dwelling purchases by owner-occupiers (3.3 per cent) and Automotive fuel (7.7 per cent). Last quarter, the annual rate of CPI increase was 3.8 per cent, which makes statements like ‘roaring back’ seem ridiculous and designed to attract headlines.’

Seems like time to call out to the prophet “…without honor, his own country” Stephen Keen – he was right in 1996-7 and 2007-8.

I’ve not heard a peep from him lately but would bet that his view of the current imbroglio would be mordant, accurate and unsweetened.

The worldwide QE, buying bonds to prop up the government and investors is the real culprit. Most of that money went into the stock market and is now spilling over in a land and property grab, a worldwide phenomenon. It is said that central banks almost have 80% of the bonds on their balance sheets. When they reach it, they can’t buy anymore, so until that time it looks sort of hunky dory. Central banks will soon have to start tapering and we all know that results in higher interest rates. Which can only result in wage demands. And before you know it you will see price rises everywhere when companies want to keep beating the profits from the year before. Unless of course central banks suddenly forfeit the repayments on the bonds they bought, or even write them off. But who will then believe the number on your piece of printed money paper ?

Conventional economics 101.

Time to switch the script.

There is only one difference, the central banks own the state bonds. Ben Bernanke might have driven the rates asked down, but basically the US is still bankrupt.

The US Dollar is the sovereign currency of the USA. They can no more run out of dollars than Coles can run out of Fly-Buys. It’s nonsense to suggest they’re bankrupt.

Given that successive governments have cooked the books in regard to the CPI, and unemployment figures, do we really have any idea what ‘inflation’ is?