Since Alan Greenspan’s two-decade reign as the chair of the US Federal Reserve, central bankers have held a mythical place among commentators and investors. This has been a triumph of spin over substance with a conga line of central bankers having done more to damage Western economies than any pandemic or national disaster ever could. While Greenspan and Ben Bernanke, his successor, are oft blamed for the global financial crisis (GFC), Australia’s own Philip Lowe looks almost certain to etch his own name into the central banker hall of infamy.

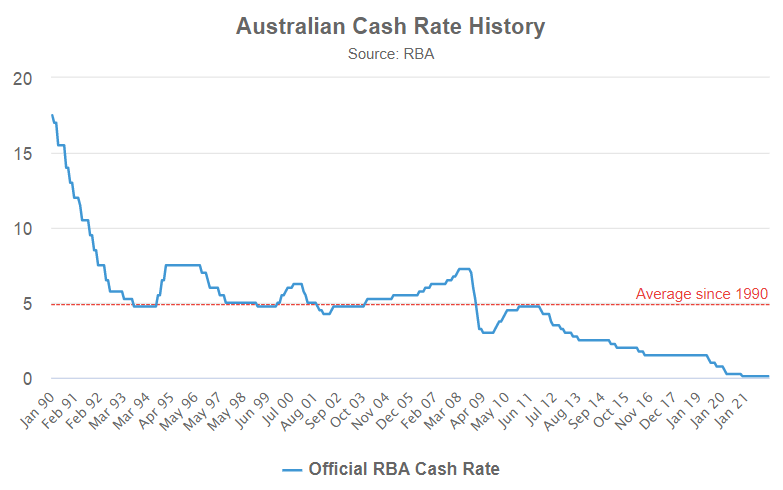

The GFC would turn Greenspan, a former Ayn Rand disciple, from saviour of the world to international laughing stock. In repeated polls, more people blamed Greenspan than anyone else for causing the GFC after he slashed rates from 6.4% in May 2000 to 1% in June 2003, inflating a massive housing bubble. The “Greenspan Put”, a mythical belief that the Fed would loosen monetary settings in periods of share market weakness, would provide his undoing.

Bernanke fared no better, utterly failing to understand the systematic risks caused by subprime lending. He managed to get almost everything he ever said wrong — the highlight being in 2006 when he infamously opined that while the “housing markets are cooling a bit”, “our expectation is that the decline in activity or the slowing in activity will be moderate, that house prices will probably continue to rise”.

The following year, just months before the financial world almost collapsed, Bernanke added, “the impact on the broader economy and financial markets of the problems in the subprime market seems likely to be contained. In particular, mortgages to prime borrowers and fixed-rate mortgages to all classes of borrowers continue to perform well, with low rates of delinquency.”

The subprime mortgage implosion would lead to the collapse of Bear Stearns and Lehman Brothers, and to trillions of dollars of taxpayer-funded largesse showered upon Wall Street.

Australia managed to avoid the worst elements of the GFC under the management of former RBA governor Ian Macfarlane. During the early 2000s, Australian rates never fell below 5% (in fact, while Greenspan was dropping rates, Macfarlane was shrewdly increasing them). This gave the RBA enough firepower to drastically cut rates during the GFC (from 7% to 3%) and then increase them as the economy rebounded.

Sadly, Macfarlane’s discipline was quickly abandoned by his successor, Glenn Stevens. Fearful of a strengthening dollar, Stevens followed the lead of the US and progressively lowered rates consistently from 2012.

Each time Australia’s grotesquely over-priced property market appeared to stumble, Stevens was there, creating his own Glenn Stevens Housing Put. In 2016, the Stevens-led RBA incredulously lowered rates to a then-record low of 1.75%, citing weak inflation and slowing economic growth (in reality, Stevens and his boomer RBA board were petrified that slowing the housing boom would crater the general economy). If only.

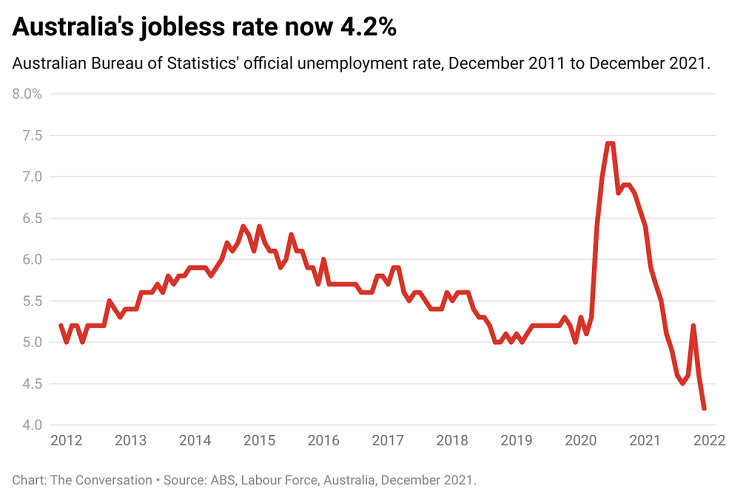

Enter Philip Lowe, who was appointed RBA governor in September 2016. For the first few years of Lowe’s tenure, he held the line (Lowe had been Stevens’ deputy since 2012), keeping official rates at a historical low of 1.75% for almost three years, despite a buoyant economy, unemployment at near-record lows of 5%, and one of the world’s most expensive housing markets.

The absurdity of Stevens’ and Lowe’s decade of ultra-low rates was that it gave the RBA absolutely no room to move in the event of an external shock — and come 2020, that shock came in the form of COVID-19.

Within months of COVID-19 hitting, Australia, like most of the world, tackled the expected calamity with an unprecedented wave of fiscal and monetary stimulus. More than $300 billion of (mostly misdirected) fiscal stimulus was created by Australia’s most proliferate former treasurer, Josh Frydenberg. But while the federal government was cashing cheques it couldn’t afford (or need), Lowe didn’t want to miss out on the fun.

With the mere thought of the property market adjusting from comically overvalued to terribly overvalued, Lowe sprung into action, slashing rates from a record low of 1.75% to only 0.25%. At the same time, the RBA lent almost $200 billion of virtually free money to commercial banks (70% went to the big four banks) to ensure the money spigots remained open. Anyone with a rudimentary understanding of how markets worked would quickly have realised this would reinflate the housing bubble. It appears Lowe, who has never worked anywhere other than the Reserve Bank itself, doesn’t fit in that category (or possibly, that was his aim all along).

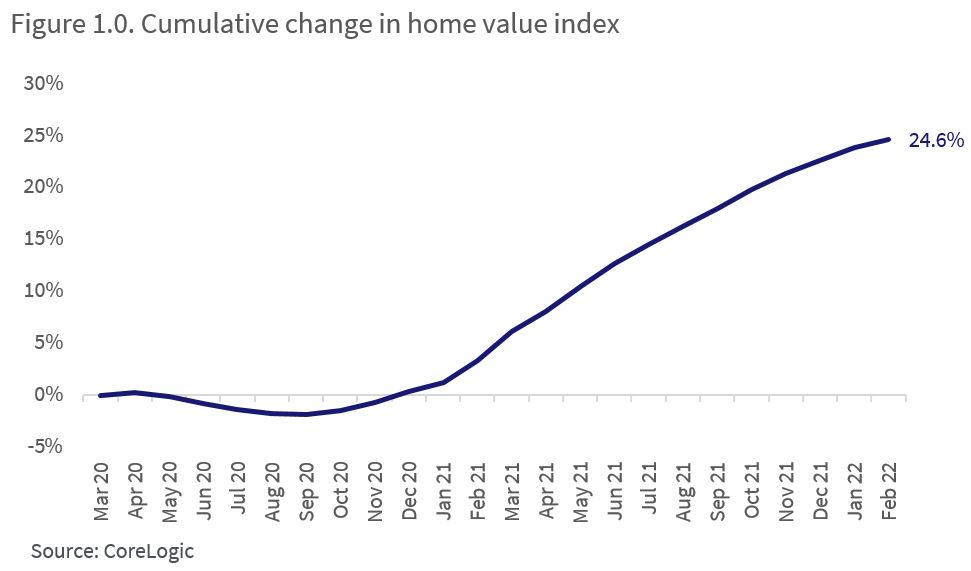

The waves of monetary and fiscal stimuli led to Australia’s already globally expensive property market rising by 24.6%. This was fantastic for baby boomers like Lowe, who already owned property, but an absolute disaster for anyone aged under forty or who didn’t already own property.

But it doesn’t end there.

By mid-2020, the Australian economy had already started to quickly recover. Unemployment would drastically drop, and by early 2021 it was nearly back to record-low levels. This was the time to quickly normalise interest rates. Alas, even as unemployment fell to only 4.5% in August 2021 and the share market hit a record high of 7629 that same month, Lowe inexplicably still failed to act.

In March of this year, even as the monstrously slow central banks around the world were urgently raising rates (New Zealand’s central bank started hiking rates in October 2021), Lowe was still sitting on his hands leaving interest rates at emergency levels. By now, inflation was already above 3%, so in real terms, Australian interest rates were negative 3.5%. This was alongside historically low unemployment, rampaging house prices and a record share market.

Make no mistake, this was Philip Lowe’s “Greenspan” moment.

It took the spectre of global hyperinflation for the RBA to belatedly act, finally raising rates in May. A succession of rises followed in June and July, taking the cash rate to 1.35%, but with inflation continuing to rise, real rates remain staunchly negative (the rate needed to quickly tame inflation in Australia is likely above 5%). In an economy where an iceberg lettuce costs $13, in real terms, it still costs savers to put money in a term deposit.

The damage caused by Lowe’s litany of failures is now being borne. The RBA will need to continue aggressively hiking rates over the coming year but is now doing so into economic weakness rather than strength. This will almost certainly tip the economy into recession.

When the list of culprits responsible for the impending economic disaster in Australia is written, Philip Lowe’s name is likely to be very near the top.

“Australia’s most proliferate former treasurer, Josh Frydenberg.”

Did you mean profligate?

Enuff! When his tenure is up next year please let the competent Ken Henry be appointed as Governor.

We have watched in increasing disbelief as interest rates dived to the point where there was no flexibility remaining. Risky & irresponsible policy.

I am incredulous that Adam appears to believe ‘incredulous’ is merely a synonym for ‘incredible’. Having read Adam in the virtual pages of Crikey for years now, I’m coming to understand that ‘columnist’ may have become a synonym for ‘illiterate’.

Hmm. this type of murdering of English makes me cringe too. In an earlier article in this issue, one of my pet peeves was visible; “there’s three problems” this sin happens daily on broadcast and print. How hard is to say “there are three problems”?

“Awaiting for approval ” cracks me up,

Tell me more about it.

or this product is for free

Yers, he’s a bit proliferate with the solecisms, ain’t he?

He has to cause a recession so he can push the unemployment rate back up. The reserve bank is a two trick pony.

This article perpetuates a dangerous Coalition myth.

The RBA has only a single lever….. interest rates.

When The madman Abbott & his Band of Incompetents took the reins and immediately started on their illusory, ideology-driven race to “Balance The Budget”, the RBA could see what effect this was having on the real economy, i.e. strangling it.

So the RBA pulled the only lever it had.

Despite their increasingly frantic (but always couched in RBA-speak) pleading for the Coalition to stop sucking out money as fast as the RBA was trying to pump it in, succesive Coalition Treasurers completely ignored them, culminating in Frydenberg’s “Back In Black” debacle…… by which time the RBA had simply run ouit of fire-power.

The economy was already on life support before COVID showe4d up and turned off the switch.

So you can thank the blind arrogance of the Coalition for the Asset price boom and the current lack of any room to manoeuvre by the RBA.

Better Money Managers my arse.

For once Adam, I sort of agree with you. I agree that central bankers have a completely unjustified mythical status all focussed on interest rates. But where we differ is that you seem to think that anyone can ever be any good at predicting the future. I agree that central bankers typically pretend they have a magical crystal ball. But the fact is in any complex environment, prediction accuracy is never better than 50% as Taleb points out and and numerous research studies by the Harvard Business School of the Bleeding Obvious and others into decision-making have proven. And that delusion leads the masses to believe that accurate prediction can occur and require that from government.

It mystifies me why more heed is not paid to the excellent Taleb idea: Stop the delusion that the future can be forecast with any useful precision. Instead, look at the actually evidence you have now and, on the basis of that evidence, do what the the evidence says produces more good and do less of what the evidence says does harm. When the evidence changes, make a new decision.

That and build much more redundancy into the system to accommodate shocks, the very opposite of neo classical economics’ fascination with ‘efficiency’.