When the famous biologist Charles Darwin visited Sydney aboard HMS Beagle in the 1830s, he noted in his diary on his first day that “the number of large houses just finished & others building is truly surprising; nevertheless every one complains of the high rents & difficulty in procuring a house”.

Housing rents are a timeless social and economic issue, though their political salience rises and falls with the macroeconomic cycle. For example, after the financially strained 1890s depression, the political pushback against the power of landlords resulted in the Landlord and Tenant Act 1899.

In 1907, the famous Commonwealth Conciliation and Arbitration Court decision in the case of Hugh Victor McKay took account of the high rents in Melbourne, which were then 20% of the typical wage, in their adjudication of a “fair and reasonable” wage. This case shows how rental markets have always generated financial challenges for households near the bottom of the income distribution who must reside in major urban centres to earn their income.

In 1911, the NSW Parliament created a select committee on the increase in house rents, which reported in 1912. This led to the Fair Rents Act 1915 and a variety of other changes to rental regulations. Like today, regulations that increased renter protections and security were argued by landlords to have “the effect of discouraging investment in rental housing”.

The federal government’s inter-state commission conducted the Piddington inquiry into housing rents in 1919, finding that the states should be in the business of building homes and that high rental prices were due to a shortage of housing (see left panel of figure 1 for news reporting at the time).

In the 1930s, multiple inquiries were conducted into housing rents, especially late in the Depression. A 1939 rents inquiry formed the backdrop to a later rent freeze that was enacted nationally due to the outbreak of World War II. Near the end of the war in 1943, the worsening underinvestment in housing led to numerous reviews, books, meetings and inquiries about how the government should actively involve itself in housing finance, land development and construction.

The postwar period was a historical anomaly when it comes to housing. The social problems arising from the degree of power of landlords over tenants were reduced by raising homeownership through subsidised housing such as war service homes, discounted private purchases of public housing, alongside rent controls and other mechanisms in the various Commonwealth-state housing agreements (CSHAs) from the late 1940s to the 1970s. Homeownership in metropolitan areas expanded from 36% prior to World War I, to 72% in 1966, which was a product of this directed government intervention to combat the problems faced by renters by making them property owners.

An important motivation in this period was to promote political stability. Liberal Prime Minister Robert Menzies desired to make households “little capitalists” and thought the “vital problem of home ownership” needed public subsidies and schemes to remedy, lest the renter household be attracted to communist ideas and tempted into political action.

But these political motives fell away by the 1970s, and the economic forces that created ongoing rental cost issues in the prewar period reemerged and persist to the present day.

For example, the 1975 review into poverty in Australia noted that households paying market rents in the private market were “[t]he group whose situation is worst after housing, and deteriorates most on a before and after housing cost comparison […]”.

Since then, dozens of inquiries into homeownership, rental prices, housing supply and other elements of the market have been conducted.

In short, the experience of housing markets in recent decades is best seen as a return to the long-run normal housing market outcome rather than a recent anomaly. This normal market outcome is that rental prices grow in line with household incomes, but often in sudden bursts at certain times in the macroeconomic cycle, leading to the displacement of renters and forced relocations for those whose incomes are not keeping up with the market.

It means that the slow but steady decline in homeownership, from 70% in 2001 to 66% in 2021, is likely to continue without non-market ways to create homeowners, which were what led to such high homeownership in the first place.

Looking at the commonalities with rental markets abroad, such as the US, UK, Canada and New Zealand, also reminds us that recent rental market dynamics that promoted the current inquiry on the worsening rental crisis in Australia are a global trend and reflect normal rental market adjustments. This only serves to reiterate the point that rental markets move with macroeconomic cycles, whether that cycle is local or global.

Real (inflation-adjusted) rents

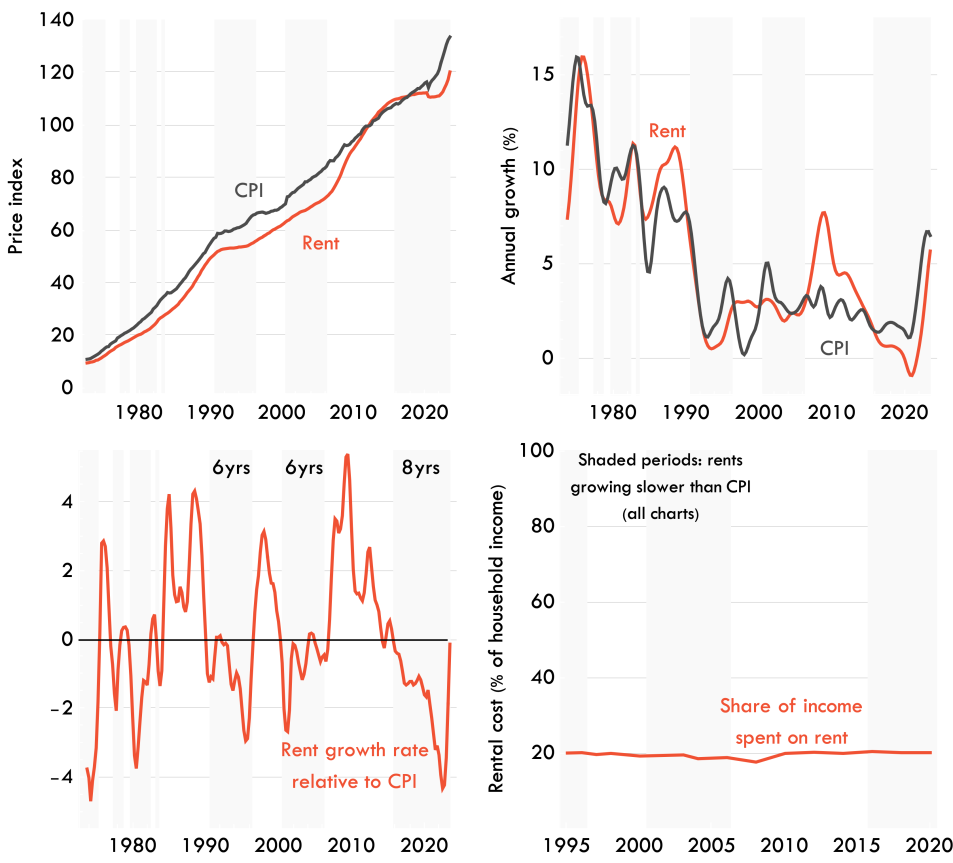

The measure of rental prices within the consumer price index (CPI) captures the price of rent paid across all renter households. A comparison between this price index and the total CPI helps show whether rents are rising faster than other goods or services, or slower, providing important context for any analysis of Australia’s rental market.

Prior to 2022, the CPI rental price index came from a “survey of approximately 4000 rental properties collected directly from real estate agents”. Since then, with automated data access, the scope has expanded to 480,000 rental properties or about 17% of the total private rental stock.

This rental price index measures the rents paid by tenants on a like-for-like basis compared with previous time periods in order to capture pure price effects (ignoring increases in quality). However, the housing stock does improve in quality over time as homes are built and old homes are renovated.

The charts in figure 2 show the CPI and the rental price index within the CPI in terms of their level (top left), their growth rate (top right), their relative growth rates (bottom left), as well as the total rent paid as a share of income for renter households (bottom right).

The following patterns are evident:

- Most of the time since 1980 rental prices have increased slower than prices for other goods and services in the CPI, but with three major cyclical adjustment periods in the late 1980s, the late 1990s, and 2006-15;

- From 2015 to mid-2023, rental prices have risen slower than prices for other consumer goods and services;

- Rent as a share of income for renter households has been flat since 1995.

Simply put, there is no evidence in the figure 2 charts of an abnormal “rental crisis” in recent years, only of normal rental markets with cyclical patterns reflecting macroeconomic conditions.

Advertised rent v paid rent

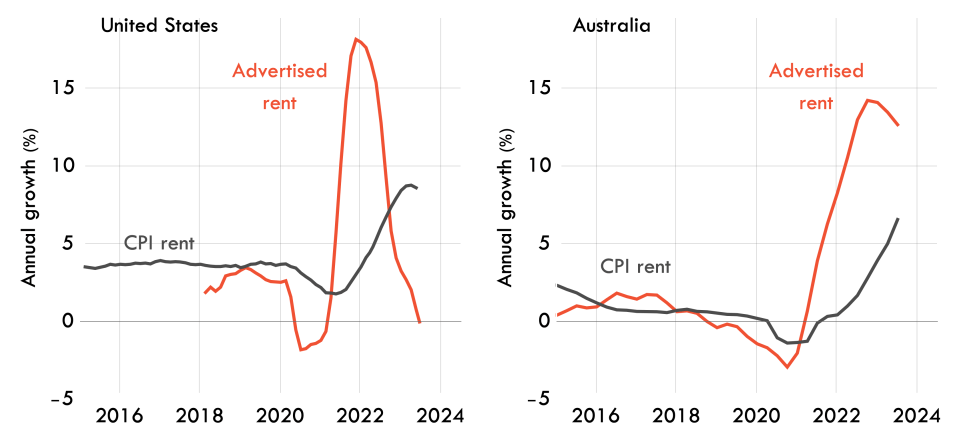

While rents paid by all renter households, measured in the CPI, have begun to increase only relative to the price of other goods and services in recent months, there are reasons to suspect that this will continue for another year at least. This is because advertised rents are a good leading indicator of rents paid in the CPI.

The difference between advertised rental prices, or prices on new leases, and the rental paid by all rental households in the CPI, is described by ABS as follows:

A useful analogy is to think about a bathtub of water. The water in the tub represents all rents being paid by households, while the water entering the tub from the tap represents new rental agreements. The CPI series is measuring the overall temperature of the bathtub whereas an advertised rents series measures the temperature of the water flowing into the tub. It will take some time for the flow of water to change the overall temperature of the water in the bathtub.

In Australia, advertised rents have surged since 2021, but the growth rate has now peaked in many areas, with declines now being seen in many cities. Rental prices in the CPI have not yet peaked and have recently started exceeding the CPI for other goods and services. However, it is unlikely that rents paid in the CPI measure will rise as fast as advertised rents have, just as they did not fall as fast during 2019 to 2021 when advertised rents fell.

Looking at the same patterns of advertised rents and all rents in the US (Figure 3, left panel) shows that rents paid in the CPI are likely to peak soon after advertised rents peak, and with lower total growth.

Rental equilibrium share of household spending

In the past three decades, rents have been 20% of gross household incomes for renter households on average (Figure 2, bottom right panel). This pattern also existed as far as we can tell in the early decades of the 20th century. In the UK, recent analysis shows that the rent-to-income ratio for renter households in the private market has been flat since 1980.

The reason for this long-run stability is because there is an economic equilibrium at play. Housing is not only a single item purchased by a household but a complete category of expenditure. When the relative price of a household consumption item falls, such as clothes or holidays, households buy more of it. Economists call this the “law of demand”, and it also applies to rental housing.

A household rents more housing by renting a larger or better-located home. Hence, when the rental price falls relative to other items, households adjust by buying more housing — in the form of bigger or better-located housing — until they spend roughly the same 20% share of their gross income on housing. This is a rental equilibrium.

This rental equilibrium is a market outcome, not an individual one, and the share of income spent on housing varies across household income levels. Lower-income households spend a larger share of income on rent, and higher-income households a lower share. But the overall market outcome, where the median household spends 20% of its gross income on housing, is an equilibrium that is persistent over long periods.

Housing supply economics

A blind spot in the many historical rental inquiries — which is likely to arise in this review — is that property owners do not have an economic incentive to build homes at a rate that pushes down housing rents and prices.

Very few submissions will present a coherent economic view of how the market for new housing operates.

Another equilibrium, the absorption rate equilibrium, is important here. Just as property owners try to optimise the density of their development projects, they also optimise the timing of them to maximise their rate of return.

As economist Tim Helm describes:

Even when it is profitable to build, it can be more profitable not to build, because development-ready land rises in value through time, and oversupplying housing means selling at a discount. The absorption rate is determined by the balance of these considerations.

Paradoxically, zoning rules can bind on each and every housing development, reducing the profits of each and every developer, without binding (constraining) the market rate of new housing supply. This is because most feasible development opportunities are rationally left undeveloped as strategic investments, in what is described as speculation or landbanking.

This means that zoning rules just shape where housing goes and what it looks like — not how much is built.

For example, if total demand growth is for six dwellings per year, zoning rules determine whether a city sees development of:

a) Six buildings with single dwellings under low-density zoning;

b) Two buildings of three dwellings each under medium-density zoning; or

c) One building of six dwellings, with other sites held vacant, under high-density zoning.

How much housing is built is a market decision.

Just like the rental market appears to be functioning as normal, so too is the new housing development market — responding to cycles, but never flooding the market and bringing down rents in a sustained way. This is why historically, even prior to planning regulations and zoning, the rate of new housing development was never sufficient to keep rents down. Despite this economic limit on how quickly new homes will be built by private property owners, there are more, bigger, better dwellings per capita in Australia in 2023 than at any point in history.

Property market symmetry

There is a deep symmetry in property markets around the absorption rate and rental equilibria outcomes. This means that any policy or regulation that benefits renters by making rents cheaper compared to this outcome comes at an equal cost to landlords.

Here’s a demonstration. In 2022, around $60 billion was paid by Australia’s renters to landlords. A hypothetical policy that reduced rents by 10% on average would save renter households $6 billion, but cost landlords the same $6 billion.

There would also be a subsequent decline in property value for landlords. It would be even larger as it is proportional to the net rental decline, not the gross rental decline. For example, if gross rent was $23,000 a year for a property, which is about the Australian average, and ongoing maintenance, tax, insurance, and other costs were $10,000, then a 10% reduction in gross rents reflects an 18% reduction in net rental income to a property owner.

How much this would affect the value of residential property assets of Australian landlords is not clear, but a rough estimate can be established. If the roughly 3 million rental homes are worth about $700,000 each — or 70% of the national average property price — then they are collectively worth about $2 trillion. An 18% price decline would wipe off $360 billion in value from the 3 million homes owned by Australia’s 1.7 million landlords.

Such enormous asset price and rental income effects are the motivation for ongoing lobbying from landlord and property interest groups against regulations that make rents cheaper.

During this inquiry, there will no doubt be many representatives of the property industry who will argue that their preferred policy changes are good for tenants. But acknowledging the symmetry of property markets means taking such proposals with a grain of salt. A landlord lobby group supporting effective rental regulations is contradicting its financial interest.

Ignoring the advice of those who benefit from higher rents and prices will go a long way to ensuring this inquiry does not meet the fate of many historical rental inquiries that ultimately sided with landlord interests and made little change.

This is a lightly edited republish from Fresh Economic Thinking by Cameron Murray.

Where do we start here? Firstly, advertised rents are not actual rents; the common and cruel practice of rent bidding is widespread, and may be skewing the stats. Secondly, the notion that rents have kept pace with the rise of other commodities is cold comfort to us renters, and merely means that we’re being gouged on all sides. The insinuation that this situation is merely cyclical could be correct, but then the recent worldwide bushfires could also be ‘merely cyclical.’

Outside of those quibbles, a good article, and a realistic assessment of how those invested in property will probably hijack the whole inquiry.

Is that Rome burning I can smell?

Why not an enquiry into housing ownership?

The reality effects of governments dropping out of supplying one of life’s (rented) necessities, to hand over same ‘responsibility’ to ‘market driven private enterprise’ on the premise that ‘they can do it cheaper and more efficiently’.

The effects of incentives such as negative gearing – to multiple-dwellings ownership portfolios and it’s real effect on market prices – especially re bidding by asset rich investors vs prospective first home owners trying to secure a foot in that door.

The effects of renting at ‘going rates’ on the ability to build a deposit for a home?

The effect of stagnant wages on the ability to build a deposit?

The possibility of changing mortgage conditions to, say, something like those of the USA (Fanny Mae/Freddie Mac)?

Thanks CM, your article beautifully outlines why govts subsidising the private rental market and/or exhorting the private market to ‘do something’ doesn’t work and will never work in a free market. And why should it. I own my property and I’ll bloody well rent it for whatever I can get for it, is a sentiment hard to argue with. It’s precisely why our govt should be looking at how it’s done OS. It’s not brain surgery. All European countries have govt housing where rents are set according to ability to pay, as we did until about 50 years ago. And frankly, labor, 30 dwellings over 5 years for the entire country as akin to doing nothing at all!

Looking at the commonalities with rental markets abroad, such as the US, UK, Canada and New Zealand, also reminds us that …….the worsening rental crisis in Australia are a global trend.

Is it global though, or is it just the ‘Anglosphere’?

Governments abdicted out of the market due to the neo liberal brain fart that began in the 80s. The scam was sold on the basis that the free market will set things right. The government and their doners already knew that the free market would in fact do exactly that and promptly set about making sure the market was not free. They manipulated the hell out of it and they still are. It is so distorted now that it will be incredibly hard to sort out. It will probably need a revolution.