The Morrison government may have secured a parliamentary majority but the Reserve Bank has voted no confidence in its economic management, taking the unusual step of flagging that it will be likely to cut interest rates at its next meeting due to concerns about unemployment.

In both a major speech yesterday by governor Philip Lowe and in the minutes of its May meeting, the bank yesterday explained that it believed there was persisting spare capacity in the economy, the rate of unemployment at which inflation would start to rise was lower than previously thought and that the jobs market was now softening. Lowe was about as blunt as a central banker could be about what the board is thinking:

We discussed a scenario in which there was no further improvement in the labour market and the unemployment rate remained around the 5% mark. In this scenario, we judged that inflation was likely to remain low relative to the target and that a decrease in the cash rate would likely be appropriate. A lower cash rate would support employment growth and bring forward the time when inflation is consistent with the target. Given this assessment, at our meeting in two weeks’ time, we will consider the case for lower interest rates.

Economists now see at least two rate cuts this year, taking rates from the current record low of 1.5% to a new record low of 1% by year’s end — or perhaps as early as July.

Noteworthy in Lowe’s speech was his view that unemployment is softening, despite more evidence of strong growth from the recent April jobs figures. That data showed the seasonally adjusted unemployment rate, in Lowe’s words, “ticked up to 5.2%” (hat-tip to Michael Pascoe for spotting that Lowe used the seasonally adjusted figure, not the trend figure that the ABS prefers in its communication) and “the underemployment rate has also moved a little higher”.

Against this was an expectation that the Coalition’s dramatically increasing tax burden on the economy would lighten a bit. “Over the past year, tax paid by households increased at a much faster rate than did income; almost 10%, compared with 3¼%,” said Lowe. “That is a big difference and it is unusual.”

According to Lowe, the bank was looking to the government’s forthcoming tax cuts to finally, if partially, fix that. “the tax offsets for low- and middle-income earners announced in the recent budget will boost disposable income.” The only problem is Morrison and Frydenberg have stuffed up the implementation of the tax offsets and these may now be delayed due to the inability to legislate them.

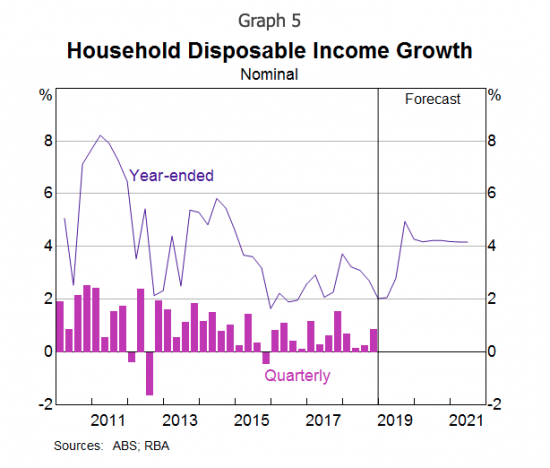

Lowe also produced a graph on household income that should shame the Coalition, given it demonstrates how bad the last few years have been for Australian families.

That’s the result of a deliberate policy of wage stagnation and the Coalition’s dramatically rising tax burden, which has seen taxes rise from 21.3% of GDP under Labor to over 23% this year.

One serious question not addressed by Lowe is why the RBA didn’t cut at the May meeting. Arguably, the case for a cut was stronger then than it will be in June: it was before the April jobs data, which showed that yes, seasonally adjusted unemployment had gone up to 5.2% but also showed continuing strong jobs growth pulling in more workers. Notable was the number of female workers, with the participation rate at a new record high, hitting 61% for the first time ever.

Was the bank worried that a rate in May would have been seen as politically problematic given there was an election campaign? Would it have been seen as a vote of no confidence in the Coalition’s economic management — exactly the issue Scott Morrison was running on?

If that was its thinking, it allowed such considerations to get in the way of fulfilling its goals. And if such politically sensitive matters were discussed, what was the role of longtime Liberal apparatchik Phil Gaetjens in them? Did he recuse himself given his close links to the Liberal Party?

Such questions shouldn’t need to be asked about the Reserve Bank, and reflect just how utterly inappropriate Gaetjens’ appointment as treasury secretary was in the first place.

Alternatively. It highlights how the RBA has never been an independent body and should be relocated back into Treasury, so that it is democratically accountable, and the poor decisions made have to be worn by the Treasurer of the day. Instead of the current farce where a ‘non-political’ body makes massively important decisions for Australian society yet the board members are unknown and unaccountable.

Hasn’t inflation be consistently below the RBA’s own target band? Isn’t this a major failing in one of their few responsibilities.

Bill Mitchell has made a good counter argument, if the RBA functions are too important for elected politicians, presumably we should do the same for all military decisions and interventions involving the actual death of defense force personnel. An independent military decision making body is clearly a must with this kind of reasoning.

Do tell me why the May meeting was not appropriate for this decision

What faith do we have that cutting the RBA rate even further will open the floodgates of investment? Has that worked in Europe with negative rates?

True, but it’s a tacit acknowledgement that the economy is on the skids, which there’d be pressure from a certain party to avoid at the May meeting

The delay in lowering interest rates or, at least, the bank rate, is not a failure to respond to employment growth in April that should leave us tut-tutting about the Reserve Bank’s lack of courage but a recognition that family income growth has been too low for too long. The fact is that the earliest possible response is not needed as Banks take their time to let the lower rate flow through and might not only trim the flow through but zero it, pleading overall borrowing costs. The rise in female employment to a record high in April just underlined the desperation felt in families at stagnation in family income, which many families are trying to fix by having women in the household work more.

The Reserve Bank also notes that the back-ended tax cut brings a rather late increase in family income and might be even more delayed if the Coalition decides to play political games by rolling their regressive tax cuts into the necessary tax cuts for lower and middle income earners.

As for business calls to legalise their underpayment of workers, that will really give the Reserve Bank something to worry about.

How about a record breaking recession later this year, brought on by the re-election of an all too business friendly government

Ian, I’m not sure about a record breaking recession at the end of the year, only the timing is in doubt, by golly it feels like something brewing. Have already moved some components of super. Into cash and bonds and may go the whole hog if the supermarket gets beyond about 6600 later this year.

When it does come, the recession we and the world have to have is going to be a doozy.

The future doesn’t look rosy, especially after Macquarie Bank revealed that one in 25 mortgage holders is in negative equity.

Perhaps Shorten did a favour to the ALP by not taking victory last Saturday. The blame for all upcoming economic woes will be borne by the Coalition, ‘the adults in charge’ for the past 6 years in the leadup.